Guide to Housing Loan Eligibility and Approval

In the Philippines, there are three home financing options: the Pag-IBIG Fund, bank loans, and in-house financing. Popular because of various plans and interest rates, bank loans are a common choice among home shoppers because they get to choose which one fits them best. Housing loans can cover the construction of a brand new residential unit; renovation projects; or the purchase of a house, condominium, townhouse, or lot.

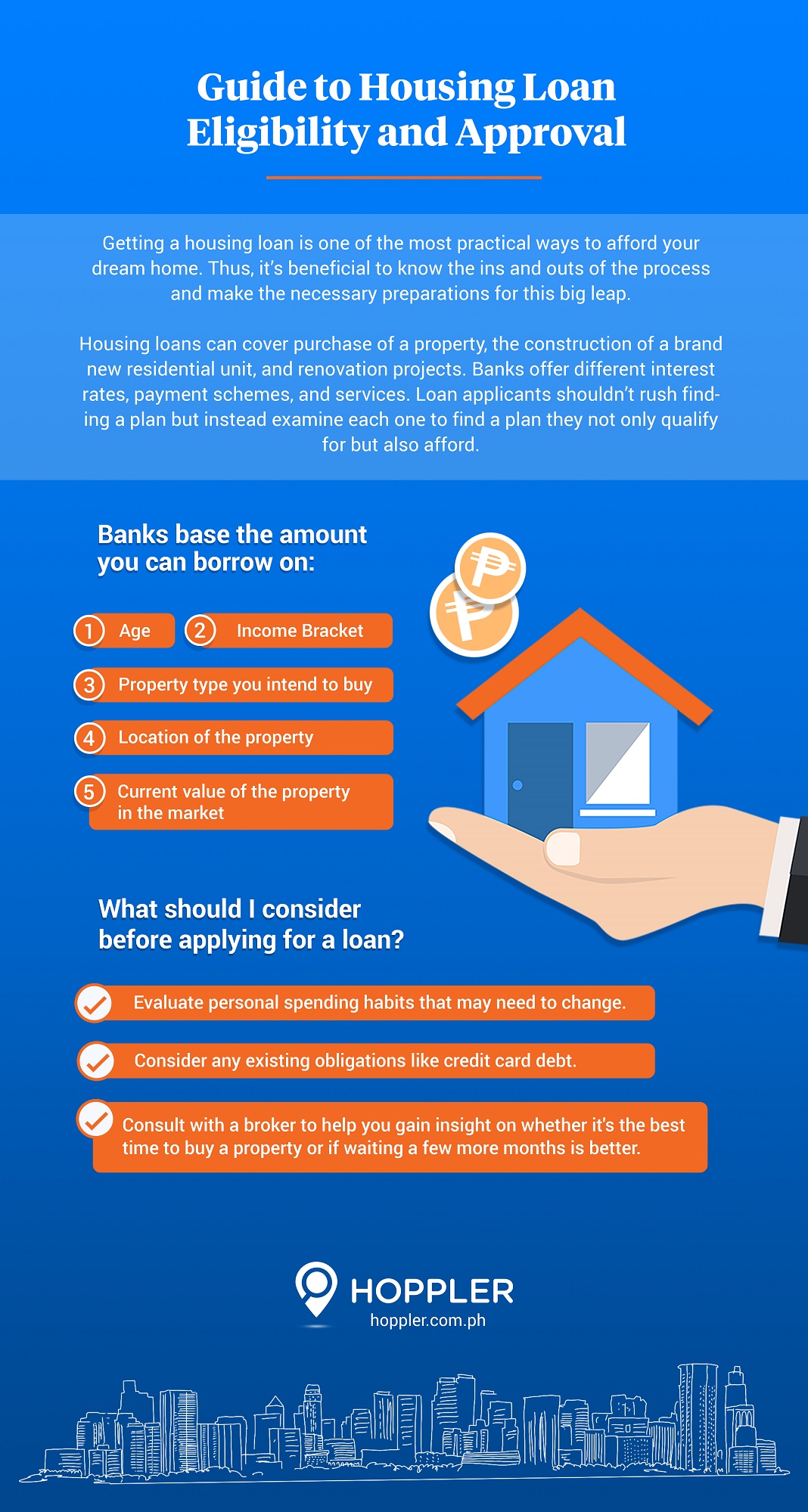

Banks offer different interest rates, payment schemes, and services. Loan applicants shouldn’t rush finding a plan but instead examine each one to find a plan they not only qualify for but also afford.

There are two types of housing loans. Conventional housing loans allow borrowers to make fixed payments over a specific period of time. Some banks offer flexible housing loans, connected to a current account, permitting the borrower to make deposits at any time. This then decreases interest charges. In most bank loans in the Philippines, you make monthly payments for the loan tenure — the period or duration for which the loan amount is sanctioned — until you’ve fully repaid both the principal and the interest.

How will my housing loan application be evaluated?

Banks base the amount that you can borrow on your age and income bracket. They also take a look at the property type and location and its current value on the market.

Income, which is perhaps the most important criteria of home loan approvals, is proof of your ability to make the monthly payments required. To get an estimate of the maximum loan amount you should only apply for based on your income, financial advisers encourage this formula. Take your annual salary after taxes and deductions then, multiply the amount by 2.5 or 3.

Why would my housing loan application be denied?

The bank may not be convinced that you have the ability to pay off the amount you intend to borrow, which is deduced based on your income. This does not necessarily mean you should give up on achieving the home you want. Instead, consider a more affordable property or apply for a loan elsewhere like the Pag-IBIG Fund.

Other times, a denied loan application could be because you’re new to your work, which serves as your primary source of funds to pay off the loan. If you’ve just started at your current job, it’ll be better to wait at least a year or two before applying for a home loan.

What should I consider before applying for a loan?

Before applying for a home loan, consider your financial capabilities and analyze your spending habits. Home loans are a big commitment and may require you to make several changes to your lifestyle.

Consider as well your existing obligations. With the loan, you’ll want to avoid falling into any debt. Avoid credit card debt, because this could also factor in to the approval of your loan.

Though an external factor, the current state of the market is something you should look at before applying for a loan. You may need to seek the expertise of a real estate broker to give you insight on variances in certain cities or neighborhoods. Your broker can help you gain insight on whether it’s the best time to buy a house or if waiting a few more months is better.

Getting a housing loan is one of the most practical ways to afford your dream home. Thus, it’s beneficial to know the ins and outs of the process and make the necessary preparations for this big leap.